![]() yyj@hf-steel.com

yyj@hf-steel.com ![]() 138 0962 7109

138 0962 7109

- 中文

2011 Steel Market Review

Click: Time:2011-12-09 00:00:00

This year, steel is facing another reshuffle. Some large players in the previous two years have all contracted their order volumes this year, with an average reduction of more than one-third. On the contrary, some small and medium-sized households have increased their inventory. Steel traders are lamenting that it is more difficult to produce steel this year than during the 2008 financial crisis. In my impression, it seems to be a three-year cycle, from 2005 to 2008, and then to this year's 11th year, under the continuous effect of monetary tightening policies, the survival situation of small and medium-sized enterprises is very severe, and the phenomenon of capital chain breakage is becoming increasingly severe.

1、 Market Trends

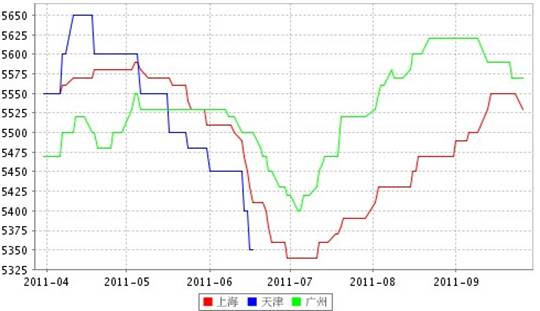

Borrowing the My Steel trend chart to see the market price trend of cold-rolled coils. (I have made one myself, but it's not as clear as this one)

(The mainstream price for cold-rolled coils in the chart is based on 1.0) We started production on February 11th this year, and the price of cold-rolled coils surged to 5700 at the beginning of the year. In less than a week, due to very weak market demand, the price fell from February 16th until the lowest price fell to 5400 at the end of March. Because the ex factory price of steel mills was very high in March, all steel mills were above 5850, which was inverted from the market by 300-400. Distributors ordered very little, and Guangdong market resources were scarce. At that time, it was very difficult for me to obtain three to five hundred tons of goods from the same distributor in the market. As a result, the price began to rise slightly to 5530 in early April, and Guangdong market began to decline again in early June. Slope up, as can be seen from the chart, it bottomed out and rebounded in early July, with the Guangdong market cold-rolled coil ************* point at 5400. Starting from July 6th, it has maintained a steady upward trend, mainly due to the bearish outlook of the cold rolling market in the early stage and long-term destocking, resulting in low inventory in the current cold rolling market. The inventory of merchants is basically kept at a low level. Under the trend of downstream demand and macroeconomic policies stabilizing, the willingness to ship at low prices has weakened, and there is a reluctance to sell. It is also reported that steel mills have comprehensively raised the order prices for September, and the ordering costs of merchants have increased. Therefore, the willingness to increase prices is strong, which has led to higher quotes. From the end of August to early September, the price of 5620 remained flat for half a month, but due to weak demand, it began to decline in mid September. By the end of September, the mainstream price of cold rolls will be 5500 yuan. For most of the year, it has been consolidating between 5400-5600 yuan, with fluctuations of around 100 yuan, leaving no room for all dealers.

The Jin Jiu market in the steel market ultimately fell through, and the escalation of the international debt crisis, the tightening of domestic funds, and the continued sluggishness of terminal demand were the main factors leading to the decline in steel prices. However, compared to other varieties, the overall performance of the cold rolling market is still acceptable. Overall, domestic inflation expectations remain strong, and the foundation for stabilizing prices is not yet solid. Once policies are relaxed, there is a possibility of a rebound, so the possibility of monetary policy relaxation is relatively small. In addition, the domestic economic growth rate has significantly slowed down, and most of the main downstream industries of steel are still operating weakly: the growth rate of railway construction has sharply declined, the construction rate of affordable housing is nearing completion, and the sales of household appliances have both declined year-on-year and month on month; The mechanical manufacturing industry is also in a declining trend and difficult to change. The relatively good anti seasonal rebound in automobile production in August is also an important support for the rebound in cold rolling. Overall, the recovery of downstream demand is much lower than previously expected. At this time, upstream raw materials such as iron ore and coke have also experienced a decline. Although the decline is limited, the downward trend is basically determined, and the cost support for steel will decrease in the later stage. At present, concerns about a decline in economic growth are becoming increasingly strong, and the inflation situation makes it difficult to loosen tightening policies. The key to whether steel prices can hold up in the fourth quarter lies in production. If steel mills cannot concentrate on reducing production, restricting production, and reducing supply, the domestic steel market in the fourth quarter will be difficult to be optimistic.

Prev : Not the end, just the beginningNext : Warm congratulations to Dongguan Hongfa Steel Structure Materials Co., Ltd. for being promoted to the first level qualification of China's steel structure manufacturing enterprise

Tel:138 0962 7109

Tel:138 0962 7109 Email:yyj@hf-steel.com

Email:yyj@hf-steel.com Fax:+86-769-86727302

Fax:+86-769-86727302 Add:Shangjiehuangjinji Industrial Park, Qishi Town, Dongguan City, Guangdong Province

Add:Shangjiehuangjinji Industrial Park, Qishi Town, Dongguan City, Guangdong Province

Copyright © 2025 All Rights Reserved Guangdong Honggang Construction Engineering Co., Ltd. 粤ICP备16029284号